Quarterly Market Comment

As an active fund manager, Octagon Asset Management prioritises high-quality research as an input to decision making. It draws on research from a range of sources, local and global. This includes research provided by Forsyth Barr. Below is its most recent Quarterly Market Comment.

Quarterly Market Comment

For the quarter ended 30 June 2026

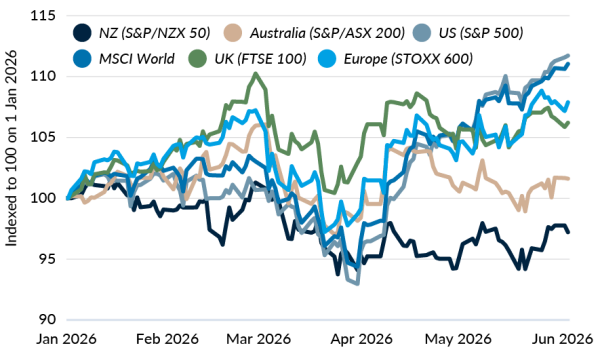

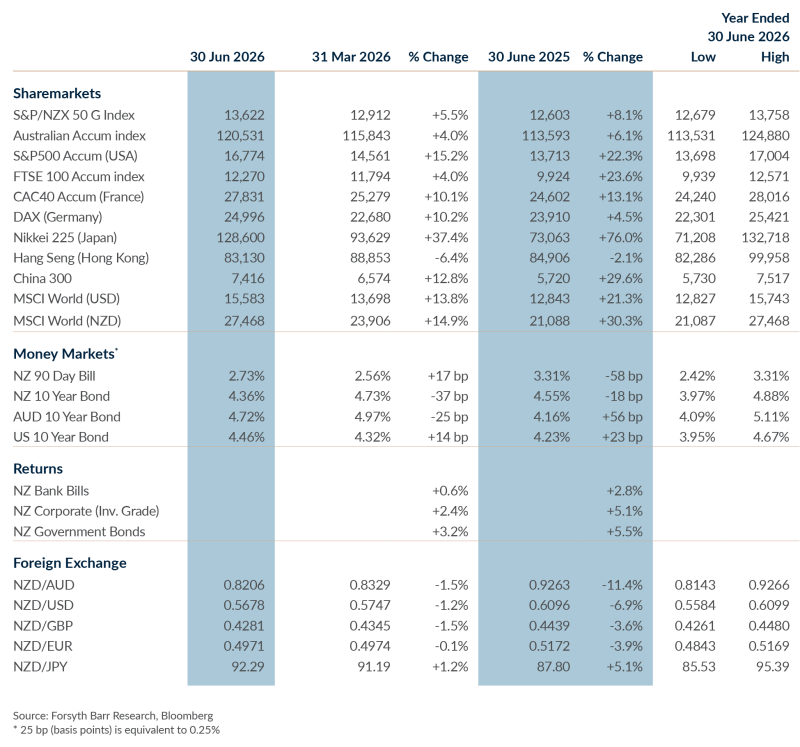

- Investment markets were broadly positive over the quarter, with global shares leading the way. The MSCI World Index rose 13.8% in local currency terms and 14.9% in New Zealand dollar terms, helped by a softer Kiwi dollar, which boosted offshore returns for New Zealand investors.

- The US market led the global gains, with the S&P 500 up 15.2% over the quarter. The recovery was supported by resilient corporate earnings, ongoing enthusiasm around artificial intelligence, and easing fears that the March energy shock would become a sustained global growth scare.

- Australian and New Zealand shares also rose but lagged the broader global rally. The New Zealand market gained 5.5% over the quarter, while Australian shares advanced 4.0%, with both indices held back by smaller relative weightings to the technology sector.

- Fixed income also delivered solid returns as inflation concerns eased and longer-term yields fell back over the quarter. NZ investment-grade corporate bonds returned 2.4%, and NZ government bonds returned 3.2%.

Middle East shock moves into the rear-view mirror

With the Middle East ceasefire holding and energy prices retreating over the quarter, investors were able to look past the March shock and refocus on company fundamentals. Shares rallied across most major regions, with the US and Japanese markets particularly strong, and the rebound extended to bonds as longer-term yields eased once the worst-feared inflation outcomes failed to materialise. It was a useful reminder that markets can react sharply to fast-moving news but also recover — often just as quickly — when the worst-feared outcomes do not eventuate.

Major equity market indices returns (indexed to 100 on 1 Jan 2026)

Source: Refinitiv, Forsyth Barr analysis

Global equity indices are increasingly concentrated in a handful of tech giants

One striking feature of this year’s rally has been just how much of it has been driven by a small group of very large technology companies. The so-called ‘Magnificent Seven’—Nvidia, Apple, Microsoft, Alphabet, Amazon, Meta, and Tesla—now account for roughly a third of the entire S&P 500, with a combined market value of around US$22 trillion. Widen the lens to the 10 largest companies and they make up close to 40% of the index. That is a higher degree of concentration than at the peak of the late-1990s technology boom, and it means a broad ‘passive’ index fund is far less diversified than many investors assume.

However, unlike many companies during the dot-com era, today’s market leaders are highly profitable and generate a large share of global corporate earnings and cash flow. Their valuations therefore rest on firmer foundations.

Even so, the risks are real. These companies share many common traits: they are large, growth-oriented, and closely tied to the artificial intelligence theme. As a result, they often rise and fall together, which can amplify gains in strong markets and losses when sentiment turns. With enormous sums being invested in AI infrastructure, competition intensifying, and high expectations already reflected in share prices, a shift in sentiment towards just a few companies could have a meaningful impact on whole market indices.

The appetite for technology exposure was clear in June, when SpaceX listed on the NASDAQ in the largest initial public offering in history. The company raised around US$75 billion at a valuation of roughly US$1.8 trillion. Its shares jumped close to 20% on debut, although they gave back some of those gains in the following days. It was a remarkable milestone, but not without controversy. The company remains lossmaking, and analysts are divided on whether the valuation can be justified. AI model companies OpenAI and Anthropic are also reported to be weighing potential listings, which may add to the market’s concentration rather than reduce it. For most investors, the key is to make sure exposure to this theme is deliberate and appropriately sized, rather than simply an accidental result of holding a broad index.

Interest rate concerns ease

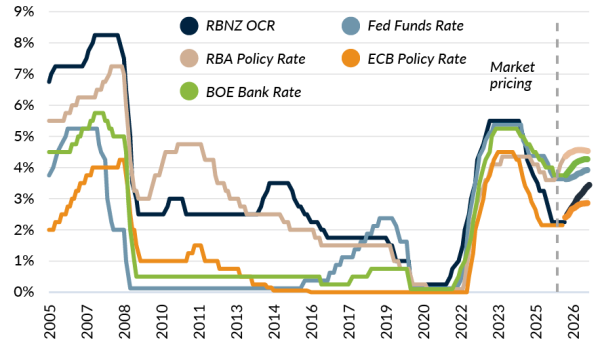

Interest rate expectations shifted materially over the quarter. When energy prices spiked, markets had begun to price in the risk that central banks would need to hike interest rates quickly to contain inflation pressures. As the ceasefire took hold and oil prices retreated, those fears faded somewhat.

In Australia, however, interest rates have already risen quickly this year. The Reserve Bank of Australia raised the cash rate by 25 basis points to 4.35% at its May meeting—the third increase this year—citing the need to bring inflation down. This weighed on parts of the Australian share market, particularly interest-rate-sensitive sectors such as property and consumer related companies.

In New Zealand, the Reserve Bank kept the Official Cash Rate at 2.25% at its May meeting. The decision was finely balanced, with the Monetary Policy Committee split 3–3 and RBNZ Governor Breman casting the deciding vote to leave rates unchanged. Interest rates are expected to move higher over the coming year, although the pace and scale of any increases will depend on how quickly the economy recovers from the oil price shock.

Central bank policy interest rates and market pricing (%)

Source: Bloomberg, ANZ, Forsyth Barr analysis

Why diversification matters more than ever

This quarter provided a clear example of why spreading risk matters. The strongest gains came from US and Japanese shares, and particularly from the technology sector. But New Zealand and Australian shares still advanced, while bonds also delivered solid positive returns as yields fell.

A portfolio spread across regions, sectors, and asset classes can capture market gains without relying too heavily on any single driver.

That lesson is especially important given how concentrated global share indices have become. With a handful of technology giants now driving so much of the market, investors who rely on a single index may be taking on more risk than the word ‘diversified’ suggests.

Holding a genuine mix of investments—including bonds, which are offering increasingly attractive income opportunities, alongside listed property and infrastructure—remains one of the most dependable ways to participate in the recovery while helping to cushion the inevitable bumps along the way.

Matt Henry

Head of Wealth Management Research

Zoe Wallis

Investment Strategist

Not personalised financial advice: The recommendations and opinions in this publication do not take into account your personal financial situation or investment goals. The financial products referred to in this publication may not be suitable for you. If you wish to receive personalised financial advice, please contact your Forsyth Barr Investment Adviser. The value of financial products may go up and down and investors may not get back the full (or any) amount invested. Past performance is not necessarily indicative of future performance.

Disclosure: Forsyth Barr Limited and its related companies (and their respective directors, officers, agents and employees) (“Forsyth Barr”) may have long or short positions or otherwise have interests in the financial products referred to in this publication, and may be directors or officers of, and/or provide (or be intending to provide) investment banking or other services to, the issuer of those financial products (and may receive fees for so acting). Forsyth Barr is not a registered bank within the meaning of the Reserve Bank of New Zealand Act 1989. Forsyth Barr may buy or sell financial products as principal or agent, and in doing so may undertake transactions that are not consistent with any recommendations contained in this publication. Forsyth Barr confirms no inducement has been accepted from the researched entity, whether pecuniary or otherwise, in connection with making any recommendation contained in this publication.

Analyst Disclosure Statement: In preparing this publication the analyst(s) may or may not have a threshold interest in the financial products referred to in this publication. For these purposes a threshold interest is defined as being a holder of more than $50,000 in value or 1% of the financial products on issue, whichever is the lesser. In preparing this publication, non-financial assistance (for example, access to staff or information) may have been provided by the entity being researched.

Disclaimer: This publication has been prepared in good faith based on information obtained from sources believed to be reliable and accurate. However, that information has not been independently verified or investigated by Forsyth Barr. Forsyth Barr does not make any representation or warranty (express or implied) that the information in this publication is accurate or complete, and, to the maximum extent permitted by law, excludes and disclaims any liability (including in negligence) for any loss which may be incurred by any person acting or relying upon any information, analysis, opinion or recommendation in this publication. Forsyth Barr does not undertake to keep current this publication; any opinions or recommendations may change without notice. Any analyses or valuations will typically be based on numerous assumptions; different assumptions may yield materially different results. Nothing in this publication should be construed as a solicitation to buy or sell any financial product, or to engage in or refrain from doing so, or to engage in any other transaction. Other Forsyth Barr business units may hold views different from those in this publication; any such views will generally not be brought to your attention. This publication is not intended to be distributed or made available to any person in any jurisdiction where doing so would constitute a breach of any applicable laws or regulations or would subject Forsyth Barr to any registration or licensing requirement within such jurisdiction.

Terms of use: Copyright Forsyth Barr Limited. You may not redistribute, copy, revise, amend, create a derivative work from, extract data from, or otherwise commercially exploit this publication in any way. By accessing this publication via an electronic platform, you agree that the platform provider may provide Forsyth Barr with information on your readership of the publications available through that platform.